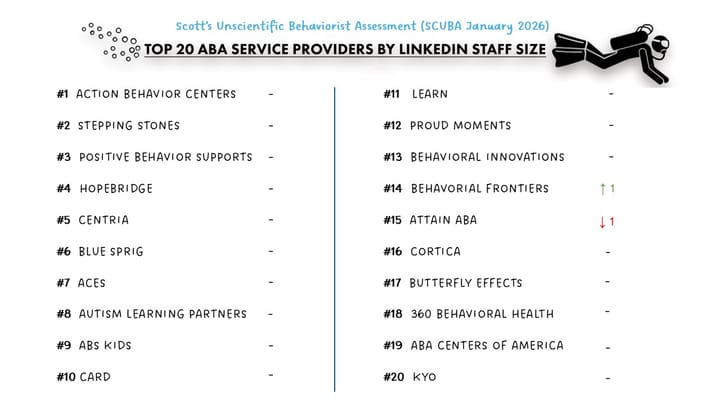

Provider SCUBA February 2026 Snapshot

Theme: The Market Is Sorting in Real Time

⚠️ Methodology Reminder

SCUBA = Scott’s Completely Unscientific Behaviorist Assessment — a deliberately imperfect, directional look at staffing momentum across ABA providers.

This is not a census. LinkedIn undercounts direct-care staff, headcount lags payroll, and public job postings reflect intent more than execution. But across 130+ organizations tracked consistently over time, these signals continue to surface meaningful structural patterns in the ABA market.

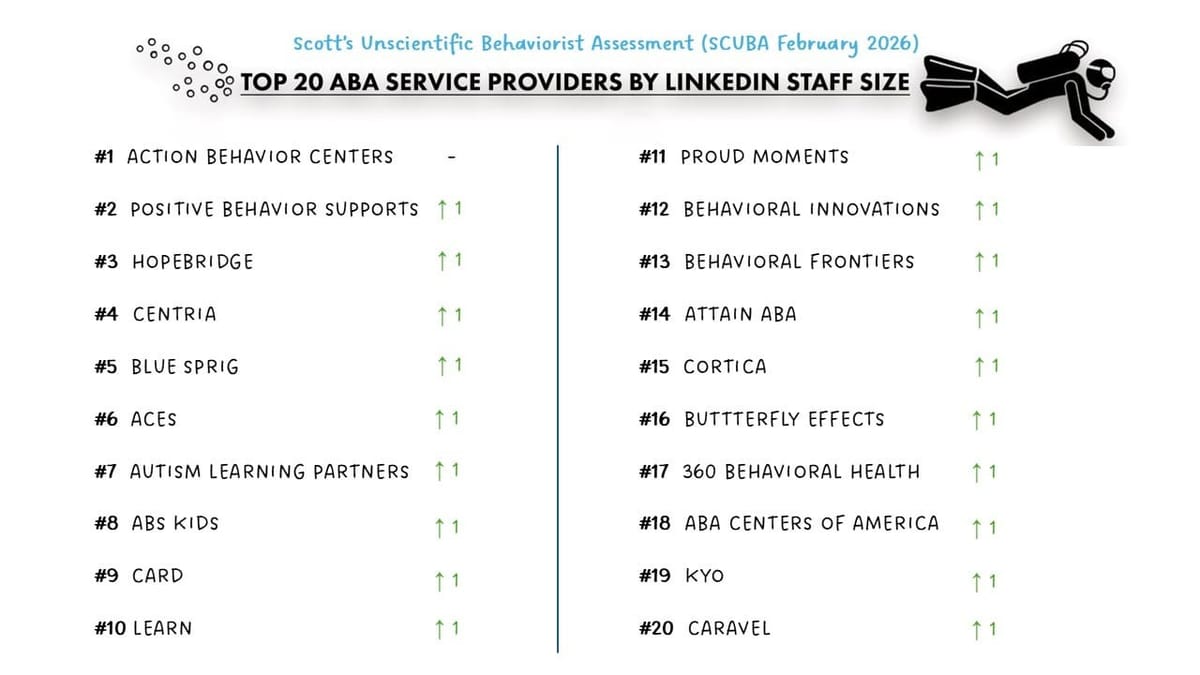

Beginning this month, the Top 20 cohort has been refined to focus on autism-first organizations — removing diversified, multiservice platforms so the signal reflects ABA-centric operating models.

February Snapshot — Closures Below, Compounding Above

February did not bring a broad slowdown.

What stood out instead was divergence.

- Some smaller, single-state Medicaid-heavy operators are closing.

- The Top 20 providers continue expanding.

- A mid-tier growth cohort is still compounding at 2–5% month-over-month.

This month reads less like a pause and more like separation.

🔀 Market Signal: Innovation Meets a Defensive Medicaid Climate

UNIFI Autism Care is winding down after three years. I’ve spoken with co-Founder & CMO Steven Merahn about the intended model: bridge pediatrics and ABA, center care on developmental domains, and build a more holistic framework for Medicaid families. I respected both the insight and the attempt to operationalize it.

The closing appears less operational than structural.

The model required payor flexibility beyond traditional fee-for-service reimbursement. At the same time, Medicaid markets increasingly appear focused on utilization control and administrative tightening — prioritizing immediate cost containment over structural innovation.

Several recent closures on the radar share similar Medicaid exposure and a growing “hammer-vs-nail” response to rising costs.

What matters:

Innovation without reimbursement alignment becomes capital-intensive — and fragile in defensive markets.

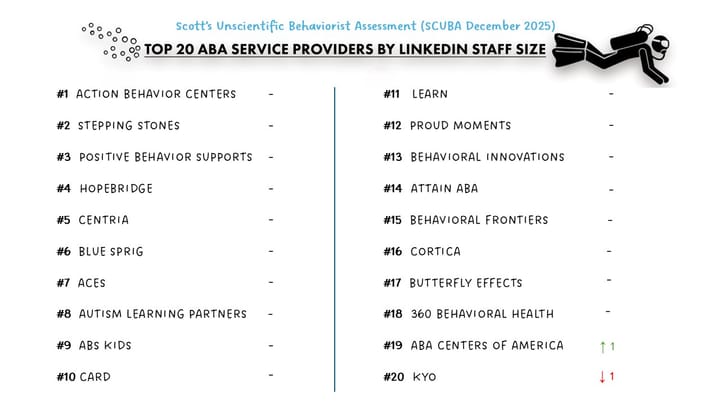

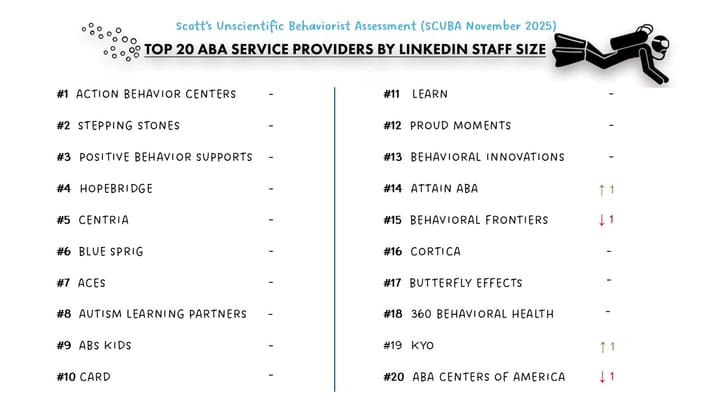

📊 Top 20 Snapshot — Expanding, But More Controlled

Month-over-month: nearly every Top 20 provider added staff.

Year-over-year: most are materially larger than February 2025.

Open job postings have moderated from mid-2025 peaks, even as total headcount continues to rise.

What matters:

Scale is absorbing volatility. Growth continues, but with more discipline.

🌱 Cohort Check: Fast-Growth Band Still Outpacing

The mid-tier cohort continues to grow faster, on a percentage basis, than the broader field:

Golden Steps ABA

SOAR

Behavioral Framework

Brighter Strides

Achievements ABA

Yellow Bus ABA

Month-over-month growth ranges roughly 2–5%.

Year-over-year growth remains materially above the Top 20 average.

What matters:

Measured expansion remains most visible in this band of the market.

🔔 Capital & Leadership Signals

• Hopebridge Autism Therapy Centers announced a CEO transition effective March 1. Dennis May steps down from his second leadership stint and LeAnne Hester steps into the role.

• Avela Health raised $10M to expand virtual autism diagnostics and remote support. A signal of continued investment into less intensive care delivery models.

Investment Observations:

M&A discussion remains elevated at industry conferences, while observable Top 20 deal volume has been relatively muted.

🚀 Hiring Snapshot — Selective, Not Re-Accelerating

Public postings remain below mid-2025 peaks.

At the same time:

total headcount continues to rise

hiring appears more targeted

large-scale, always-on postings are less visible

What matters:

Hiring has not stalled, in spite of Medicaid headwinds. It has become more deliberate.

SCUBA Takeaways — February 2026

- Medicaid strain is surfacing at the lower tier

- The autism-first Top 20 continue expanding

- Mid-tier operators are still compounding

- Capital and leadership shifts signal repositioning

- Hiring is selective, not aggressive

The ABA market isn’t contracting.

It’s sorting — by capital depth, payor alignment, and operational discipline.

If you’re navigating these shifts — whether as a provider, platform, or investor — let’s connect. Interested in keeping pace with Tech, Ops and Data content? 👉 Subscribe here