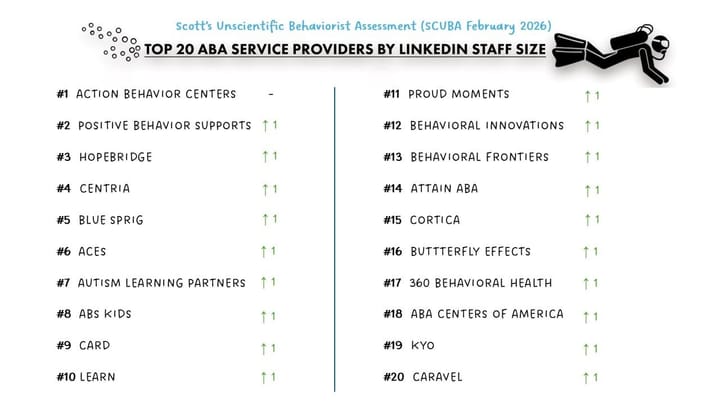

Provider SCUBA January 2026 Snapshot

Theme: Where Last Year’s Decisions Are Showing Up in Operations

⚠️ Methodology Reminder

SCUBA = Scott’s Completely Unscientific Behaviorist Assessment — a deliberately imperfect, directional look at staffing momentum across ABA providers.

This is not a census. LinkedIn undercounts direct-care staff, headcount lags payroll, and public job postings reflect intent more than execution. But across 130+ organizations tracked consistently over time, these signals continue to surface meaningful structural patterns in the ABA market.

January Snapshot — Quiet Month, Clear Signals

January brought relatively little headline news.

What stood out instead was where decisions made over the past year are now surfacing — in staffing patterns, service mix, and day-to-day execution.

This month reads less like a turning point and more like a reveal.

🌬️ Market Signal: Pressure Is Landing in Mechanics, Not Rates

Across markets, payor and regulatory pressure is showing up less through visible rate action and more through how care is administered:

- tighter definitions around supervision and caregiver involvement

- increased scrutiny on authorized hours and documentation

- longer credentialing, reauthorization, and claims cycles

None of these are new individually. What’s notable is how consistently they are now shaping workflows.

What matters:

Access and margin are increasingly determined by operational mechanics, not contract terms.

🌱 Cohort Check: Mid-Tier Operators Still Carrying Momentum

A familiar cohort of mid-sized providers — outside the Top 20 — continues to account for a disproportionate share of visible hiring momentum.

This group includes:

- Achievements ABA

- Yellow Bus ABA

- Behavioral Framework

- Golden Steps ABA

- Brighter Strides ABA

- Akoya

Over the past three months, this mid-tier cohort’s LinkedIn headcount grew roughly 2× faster than the rest of the tracked provider set.

Common traits continue to show up across this group:

- disciplined regional expansion

- repeatable de novo execution

- steady, non-reactive hiring

- enough scale to invest in operations without the legacy burden of the largest platforms

What matters:

Measured growth remains most visible in this band of the market.

🔀 Service Mix Is Starting to Split by Scale

One of the clearest differences right now is how providers are handling OT, ST, and PT.

Smaller providers are still using multidisciplinary services as a growth lever. Providers like KidsChoice are expanding OT and speech alongside ABA to deepen referral relationships and improve the family experience while organizational complexity remains manageable.

Larger platforms are moving differently.

Following its acquisition of Ally Pediatric Therapy, ACES is unwinding in-house OT, ST, and feeding services and shifting to external care coordination — tightening focus around an ABA-centric operating model.

What matters:

Multidisciplinary breadth can be accretive early. At scale, some providers are choosing simplification over scope.

🚀 Hiring Snapshot — Selective, Not Re-Accelerating

Public job postings appear more restrained than peaks observed in mid-2025.

At the same time:

- total headcount across the dataset continues to rise

- hiring looks more targeted and role-specific

- fewer always-on postings, more deliberate adds

What matters:

Hiring hasn’t stalled. It has become more intentional.

SCUBA Takeaways — January 2026

- Operational mechanics are where last year’s decisions are now landing

- Mid-tier providers continue to outpace the broader field on momentum

- Service mix strategies are diverging by scale

- Hiring is selective, not aggressive

- The market is sorting by who can absorb complexity — and who can’t

The ABA market isn’t pausing.

It’s revealing the downstream impact of choices already made.