Provider SCUBA March 2026 Snapshot

⚠️ Methodology Reminder

SCUBA = Scott’s Completely Unscientific Behaviorist Assessment — a deliberately imperfect, directional look at staffing momentum across ABA providers.

This is not a census. LinkedIn undercounts direct-care staff, headcount lags payroll, and public job postings reflect intent more than execution. But across 130+ organizations tracked consistently over time, these signals continue to surface meaningful structural patterns in the ABA market.

🤿 March Snapshot — Growth Continues, But Has Slowed

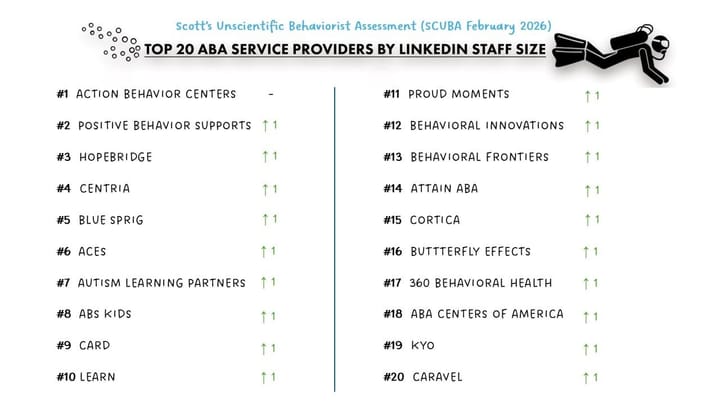

March did not show a slowdown in headcount.

It showed a slowdown in momentum.

Across the Top 20:

- Most providers added staff month-over-month

- Gains were incremental, not step-change

- Job postings remain below mid-2025 peaks

Quarterly context (Jan → Mar):

- Top 20 average growth: 3.2%

This is lower than prior periods where growth was more aggressive.

What matters:

Growth continues—but has shifted to steady, controlled expansion.

🔀 Market Signal: Fraud, Waste & Abuse Focus

ABA has entered a more visible phase, driven by OIG audits and recent reporting.

- Oversight of billing, documentation, and utilization is expanding

- Rapid Medicaid growth is drawing policy attention

- Variation in care models and therapy intensity is becoming more exposed

In response, some states are taking a “hammer vs. nail” approach:

- broad rate resets

- service caps

- tighter utilization controls

What matters:

The system is being simplified in response to variability—

even where care delivery is not.

📊 MVP Cohort — Fastest % Growth (Q1 2026)

This month introduces a new lens:

MVP Cohort = the five providers with the highest percentage headcount growth (Jan 2026 → Mar 2026)

This cohort will reset each quarter, then be tracked month-to-month to compare how recent high-growth providers perform against the Top 20 and each other.

It answers a different question than scale:

not who is largest—but where momentum is building.

MVP Cohort — Q1 2026:

- Achievements ABA

- Brighter Strides

- SOAR

- Behavioral Framework

- Golden Steps ABA

Cohort performance:

- Average growth: 11.0% for the quarter

- More than 3x the Top 20 growth rate (3.2%)

Where they sit:

- Largely within the next tier below the Top 20 (often in the Top 50 by LinkedIn staff count)

- In active expansion phases rather than optimization

What matters:

- Growth leadership is not concentrated at the top

- The fastest-moving providers are building regional density below the top tier

- Tracking this group over the next quarter will show which sustain momentum—and which converge back toward the market

Provider SCUBA Takeaways — March 2026

- Quarterly growth slowed to 3.2% at the top tier

- Fraud, waste, and abuse scrutiny is becoming central

- Some states are responding with broad cost controls

- The fastest-growing providers are concentrated in the mid-tier, not the top

If you’re navigating these shifts — whether as a provider, platform, or investor — let’s connect.

Interested in keeping pace with Tech, Ops and Data content? 👉 Subscribe here