Provider SCUBA June 2026 Update

⚠️ Methodology Reminder

SCUBA = Scott’s Completely Unscientific Behaviorist Assessment — a deliberately imperfect, directional look at staffing momentum across ABA providers.

This is not a census. LinkedIn undercounts direct-care staff, headcount lags payroll, and public job postings reflect intent more than execution. But across 130+ organizations tracked consistently over time, these signals continue to surface meaningful structural patterns in the ABA market.

🤿 June Snapshot — Scale without Compression

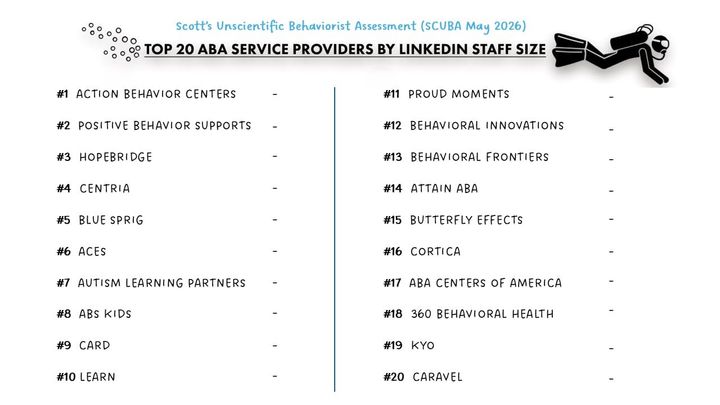

Action Behavior Centers surpassed 9,000 LinkedIn employees in June while adding nearly 600 employees during Q2.

At that scale, percentage growth compression is almost universal across the market. Large organizations simply have more denominator to fight against.

Action doesn't appear to have gotten that memo.

The growth rate they're posting is more consistent with a provider in the 500–1,500 employee range than one approaching 10,000. That's not a rounding error. And it hasn't been a single quarter. The momentum has been consistent across the last two years with no obvious hiring spike or acquisition that explains it.

At some point, sustained outperformance stops looking like noise and starts looking like signal.

📊 MVP Cohort — Quarter Two

When the Q1 MVP Cohort was introduced, the question was simple: one exceptional quarter, or something more durable?

Three months later, three of the original five providers qualified again.

Q2 2026 MVP Cohort

- Behavioral Framework (repeat)

- Golden Steps ABA (repeat)

- Brighter Strides ABA (repeat)

- ABA Centers of America (new)

- Action Behavior Centers (new)

The three returning providers continued outperforming the broader market. Behavioral Framework accelerated. Golden Steps maintained nearly identical growth. Brighter Strides continued posting strong gains.

ABA Centers of America qualified on staffing momentum. Since the June census, reporting has surfaced layoffs and legal disputes with major payors. It will be interesting to see how that shapes their Q3 trajectory.

The remaining Q1 cohort members continued growing, though no longer at MVP pace.

📈 Hiring Snapshot — Growth Continues Despite the Noise

This is perhaps the most counterintuitive data point in the June snapshot.

Industry conversation throughout Q2 has been dominated by Medicaid reimbursement pressure, utilization scrutiny, authorization management, and the general sense that the operating environment is tightening.

If you spent time at AIS West or CASP, you heard some version of this in nearly every room.

The staffing data tells a different story.

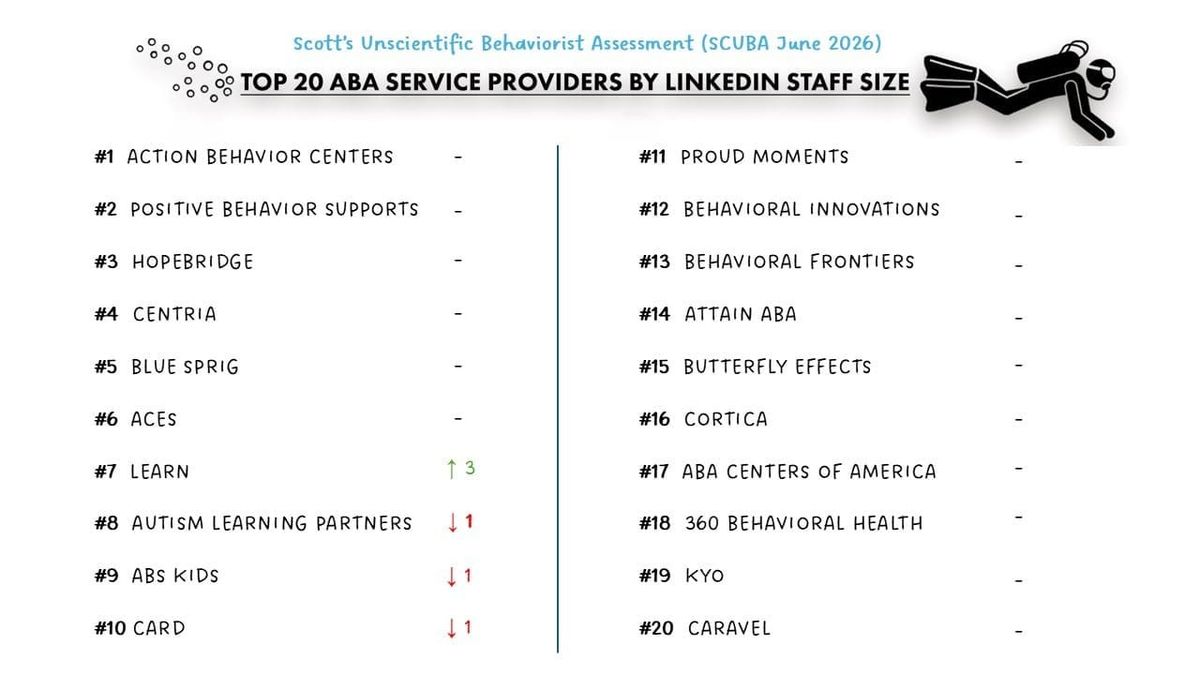

All but one of the Top 20 added LinkedIn headcount from May to June. Average Q2 growth across the dataset was 4.2%.

That's not a market bracing for contraction. That's a market that continues to hire with apparent confidence in future demand.

The disconnect between provider sentiment and provider behavior has now persisted long enough to be worth naming directly. Organizations may be more cautious in how they talk about the environment. They are not yet being more cautious in how they staff into it.

Whether that gap eventually closes — and in which direction — remains the most important question the data will answer over the next two quarters.

The market continues to grow.

Increasingly, the differentiator isn't simply scale.

It's the ability to sustain momentum as organizations become larger and the operating environment becomes more demanding.