📬MissionViewpoint Monthly Update – March 2026

The Mission of MissionViewpoint

👉 To drive more—and better—access to autism care through the smarter use of technology and data.

Welcome to the ABA Mission Viewpoint March 2026 Monthly Update

Theme: Why Autism Care Is Ripe for Consolidation — and Why It Keeps Failing

Two developments this month brought the autism care system into sharper focus.

First, a series of Wall Street Journal articles on Medicaid autism billing exposed extreme spending outliers and reignited scrutiny of how the sector is governed.

Second, Centene’s decision to divest Magellan Health at a loss underscored how difficult autism cost volatility remains to manage—even inside vertically integrated insurance organizations.

Taken together, these signals point to the same underlying tension.

Demand for autism services continues to rise.

Private capital remains interested in the sector.

But the infrastructure required to govern, measure, and integrate autism services is still uneven.

That gap helps explain why consolidation in autism care has proven so difficult.

Over the past month, MissionViewpoint examined the issue from four structural angles:

• the platform layer

• clinical alignment

• transaction structure

• operating reality after acquisitions

Across providers, platforms, and investors, the pattern is consistent: the barriers to consolidation rarely begin with dealmaking. They emerge from the operational, clinical, and governance realities that follow.

The first signal surfaced in the media.

📰 The Governance Gap Behind the WSJ Stories

The recent Wall Street Journal articles about autism Fraud, Waste, and Abuse sparked intense discussion across the field this month.

Some of the examples described are simply egregious. When vulnerable populations are involved, providers carry a heightened obligation to operate with integrity, and some behavior highlighted clearly failed that standard.

At the same time, the cases highlighted appear to represent extreme outliers rather than the operating norm across the autism provider landscape. Most organizations delivering ABA services operate under substantial regulatory, clinical, and operational constraints.

What the reporting ultimately exposed is something broader: a governance system that has not kept pace with the scale of autism care.

In several states, Medicaid oversight frameworks appear misaligned with basic healthcare reimbursement norms. Rate structures, authorization controls, and documentation standards sometimes allowed providers unusually wide latitude compared with other medical services. That environment does not exist everywhere, but variation across states remains substantial.

Part of the challenge is structural. Governance is inherently difficult in a field where widely accepted outcome measures—recognized by payors, providers, regulators, and families—are still evolving.

When demand expands faster than the infrastructure used to monitor it, extreme outliers eventually surface.

The likely response is not the disappearance of autism services, but tighter authorization frameworks, improved data instrumentation, and greater operational visibility across providers and platforms.

In other words, the sector is entering a period of institutional maturation.

And that shift connects directly to this month’s theme: Why autism care appears ripe for consolidation—and why it continues to prove so difficult in practice.

Angle 1 — Platform Risk - When the Autism Tech Stack Becomes the Risk

The first analysis examined the infrastructure beneath consolidation itself: the autism technology stack.

Over the past several years, significant capital has flowed into software platforms supporting autism providers. But valuation compression across vertical healthcare software, combined with fragmented outcome frameworks and evolving care models, has introduced new uncertainty into that layer.

Under those conditions, the first rationalization wave in the sector may occur in software platforms before it occurs in provider roll-ups.

Takeaway:

If the technology infrastructure supporting autism providers remains fragmented and unstable, consolidation at the provider layer becomes harder—not easier.

Read: When the Autism Tech Stack Becomes the Risk

Angle 2 — Clinical Alignment - The Cost of Variable Care Logic

The second analysis explored the deeper structural constraint beneath provider consolidation.

Healthcare sectors that consolidate successfully typically share common operating logic: standardized care pathways, aligned outcome frameworks, and predictable revenue models.

Autism care does not consistently have these.

Providers vary widely in clinical philosophy, supervision design, intensity assumptions, and outcome measurement. Without shared operating logic, scale multiplies variation rather than reducing it.

The same variability complicates actuarial modeling at the payor level, as illustrated by Centene’s recent Magellan divestiture.

Ownership alone cannot resolve that misalignment.

Takeaway:

Without shared clinical frameworks and outcome definitions, scale multiplies variation rather than creating efficiency.

Read: Why Autism Care Is Ripe for Consolidation — and Why It Keeps Failing

Angle 3 — Transaction Structure - Deal Activity vs Deal Consolidation

Autism services continues to generate significant deal activity—but activity alone does not equal consolidation.

Recent transactions have largely taken the form of:

• sponsor-to-sponsor platform transfers

• regional tuck-in acquisitions

• minority recapitalizations

• exploratory sale processes

These transactions create liquidity and expansion. What they rarely produce are mergers between large providers—the type of integration that typically defines consolidation phases in other healthcare sectors.

The governance environment is also tightening. As Medicaid programs respond to OIG audit findings and public scrutiny, acquirers are inheriting not only clinics and contracts but also the documentation practices and compliance exposure embedded in those operations.

This makes integration risk harder to underwrite and reinforces the caution already visible in transaction structures.

Takeaway:

Deal activity continues across autism services, but most transactions expand platforms rather than integrate them—leaving true consolidation largely unrealized.

Read: Autism M&A Is Active — But True Consolidation Still Hasn’t Arrived

Angle 4 — Operating Reality - When Consolidation Meets Operating Reality

The final analysis examined what happens after acquisitions occur.

Most providers do not operate on intentionally designed enterprise systems. Instead, they run on accumulated technology tools, localized workflows, and institutional knowledge embedded in individuals.

When acquisitions occur, those systems collide.

Tech sprawl, process debt, regulatory variance, and compliance exposure transform integration from a migration exercise into forensic reconstruction.

The recent federal and media scrutiny of autism billing highlights why this matters. When documentation expectations differ across states and payors—and when those expectations are not validated until after claims are submitted—providers can find themselves exposed to audits even when care was delivered in good faith.

Integration effort behaves less like a temporary project and more like a standing operating function.

Takeaway:

Integration challenges rarely stem from strategy alone—they arise from accumulated workflows, technology sprawl, and regulatory complexity that were never designed to merge.

Read: Provider Consolidation Reality: Why Value Breaks Before It’s Realized

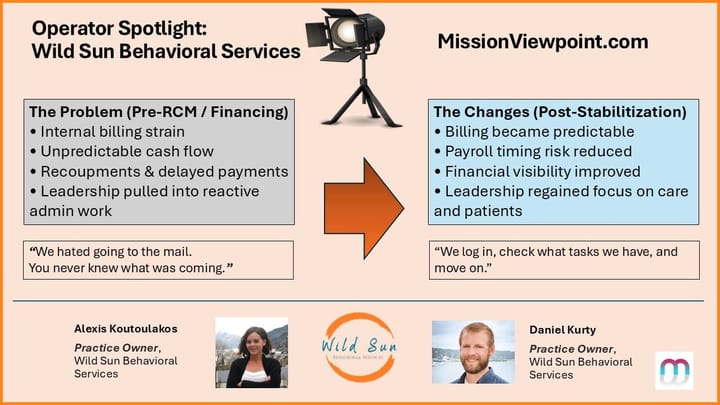

💡Operator Spotlight: Wild Sun Behavioral Services

This month’s spotlight highlights Wild Sun Behavioral Services, a Colorado provider focused on protecting a human-centered care model rather than pursuing aggressive expansion.

Founders Daniel Kurty and Alexis Koutoulakos built the practice around a simple philosophy: relationship is the primary reinforcement. Growth followed organically, but operational strain quickly surfaced behind the scenes.

Like many small providers, Wild Sun discovered that billing volatility—not clinical complexity—posed the greatest threat to sustainability. Denials, recoupments, and delayed reimbursements made cash flow unpredictable and pulled leadership attention away from care.

To stabilize operations, Wild Sun partnered with Camber to improve billing visibility before claims were submitted, while Flychain provided claim-based financing and financial management tools that reduced the stress created by reimbursement delays.

The result was not faster growth, but operational breathing room—allowing leadership to refocus on staff development, clinical quality, and a new nonprofit education initiative.

Wild Sun’s experience highlights a quieter truth in autism care: sometimes technology doesn’t enable scale. It simply allows mission-driven providers to keep doing the work they set out to do.

Read: Operator Spotlight: Wild Sun Behavioral Services

✅ Platform Highlights

Platform activity moderated in February as the ecosystem entered conference season.

Major feature launches were limited. A few developments are worth noting:

• Rethink expanded its Behavioral Health Marketplace integration with Brellium, embedding automated documentation QA directly into clinical workflow.

• Motivity added denial code–to–denied amount mapping and bulk transfer of billed appointments, improving visibility into revenue cycle friction and payor interactions.

• Frontera Health released a free parent-facing support app, extending behavioral guidance beyond the clinic environment.

• EarliPoint Health announced support for a $21.9M longitudinal study at Marcus Autism Center, tracking 7,500 children across behavioral, brain, and genomic measures.

• Artemis ABA introduced bulk session note downloads, highlighting growing demand for documentation portability.

📊 Provider Trends

Closures are beginning to surface among smaller, Medicaid-heavy providers as reimbursement and administrative pressure tighten.

The autism-first Top 20 providers continue expanding, though visible acquisition activity at that level remains limited.

A fast-growing mid-tier cohort — including Golden Steps, SOAR, Behavioral Framework, Brighter Strides, Achievements, and Yellow Bus — is beginning to pursue selective acquisitions alongside de novo growth.

Hiring remains active but more targeted than during the 2024–2025 expansion cycle.

Takeaway:

Consolidation is beginning to appear — just not where most observers expected it.

💬 Closing Thoughts

Viewed through the platform layer, clinical alignment, transaction structure, and operating reality, the same pattern appears repeatedly.

Autism services expanded rapidly over the past decade. Access improved. Capital entered the sector. New delivery models emerged.

But the systems required to govern, measure, and integrate that expansion have developed more slowly.

The Wall Street Journal stories highlighted gaps in oversight and reimbursement controls across the Medicaid autism system.

Centene’s Magellan divestiture highlighted how difficult autism cost variability remains to model even inside vertically integrated insurance organizations.

Provider consolidation continues to stall under the weight of operational and clinical misalignment.

Taken together, these signals suggest the sector is entering a new phase.

The next stage of autism care will not be defined primarily by expansion. It will be defined by institutional maturity — whether providers, platforms, payors, and regulators can build the systems and processes required to support the scale that already exists.

Until those systems strengthen, consolidation will continue to appear inevitable on paper while remaining difficult in practice.

In April: Why Autism Care Is Ripe for Consolidation—and Why It Keeps Failing.

Until next time,

— Scott

P.S. Know someone shaping ABA operations, technology, or investment? Invite them to subscribe at missionviewpoint.com.