Motivity’s Calmanac Acquisition Is About More Than Practice Management

Last year, when Five Elms Capital invested $27M into Motivity, I wrote that the underlying strategic question was not the investment itself, but whether Motivity intended to evolve beyond a clinical platform into broader operational infrastructure for autism care organizations.

This week's announcement provides a much clearer answer.

Motivity has signed a definitive agreement to acquire Calmanac.

Structurally, this may be one of the more important acquisitions the autism technology market has seen over the past year — across both providers and platforms.

- not because "all-in-one platforms" are new.

- not because practice management consolidation is surprising.

- and not because providers were explicitly demanding another single-vendor stack.

The significance is what this says about where the market itself is moving.

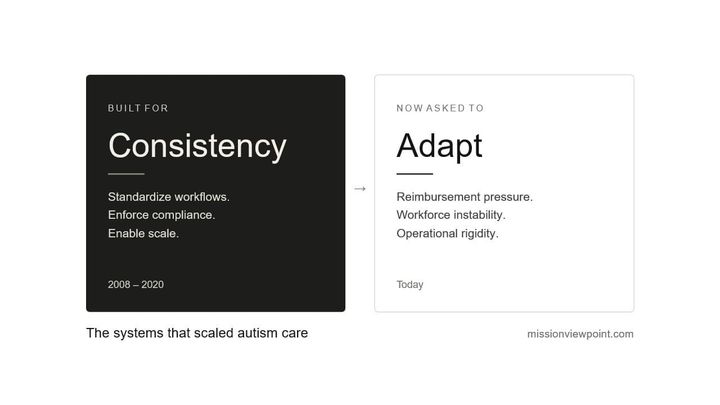

Why End-to-End Infrastructure Matters More Now

Historically, many ABA platforms began around clinical documentation and session data collection.

Over time, the market partially bifurcated:

- some platforms stayed primarily in the clinical lane,

- while others expanded further into scheduling, billing, authorizations, and broader practice management infrastructure.

For years, that separation was mostly workable.

But many of the platforms that expanded operationally also accumulated technical limitations that made enterprise adaptability increasingly difficult:

- fragmented data models,

- limited interoperability,

- constrained reporting,

- and architectures not originally designed for modern enterprise data accessibility.

Those limitations helped create the 2024-2025 investment thesis behind newer SaaS platforms - including companies like Lumary, Passage Health, Hipp Health and Motivity - that positioned more modern architectures as potential alternatives to legacy ABA infrastructure.

But the environment is also changing.

As reimbursement pressure rises and utilization scrutiny increases, the boundary between "clinical" and "back office" infrastructure is starting to blur.

Prior authorization is a good example.

Historically, prior auth functioned primarily as an administrative workflow. Increasingly, it may begin behaving more like an ongoing operational intelligence function - requiring tighter coordination between clinical documentation, authorization history, staffing, reporting, and payor-facing visibility.

Platforms are increasingly being evaluated not simply on whether they complete workflows, but on whether they can connect operational, financial, and clinical context into a coherent longitudinal system.

That shift naturally favors platforms attempting to unify more of the operational surface area.

This Acquisition Is Really About Enterprise Operational Infrastructure

This acquisition likely moves Motivity into a very small category of ABA platforms with meaningful exposure to true enterprise-scale operational complexity.

Many platforms function well for smaller or mid-sized providers. Far fewer have demonstrated the ability to support:

- multi-state operations,

- enterprise credentialing,

- sophisticated reporting,

- large-scale scheduling,

- and highly customized payor workflows.

Depending on how one defines "proven," there may be fewer than a handful of ABA platforms with meaningful operational exposure at something resembling top-10 provider scale.

From the outside, the Motivity + Calmanac fit is logical.

Motivity already had:

- strong clinical credibility,

- meaningful BCBA adoption,

- favorable therapist usability,

- and growing positioning around analytics and enterprise data accessibility.

What it lacked was a mature operational backbone capable of competing at the enterprise workflow layer.

Calmanac appears to provide that.

But what makes this more than a feature acquisition is where Calmanac was built.

CARD has been one of the most organizationally dynamic providers in the history of autism care. Leadership changes. Ownership transitions. Restructurings. Recapitalizations. Through all of it, CARD remained a top-10 provider — and Calmanac ran through all of it.

That means the platform was not shaped by a clean, stable environment. It was tested under sustained enterprise-scale operational stress across multiple ownership cycles at a scale very few ABA platforms have ever experienced firsthand.

The emphasis on:

- compliance-aware scheduling,

- credentialing logic,

- payor-aware workflows,

- enterprise bulk operations,

- and rules-based operational constraints

reflects a platform philosophy forged under that pressure — not retrofitted to it.

That operational history may matter more than the PM feature set itself.

Because the strategic challenge in ABA is increasingly not just:

"Can the software complete workflows?"

But:

"Can the infrastructure support enterprise operational adaptation over time?"

That increasingly depends on:

- interoperability,

- enterprise data access,

- migration feasibility,

- operational visibility,

- and architecture capable of supporting enterprise-scale complexity.

Many of the API and data-access limitations providers experience today are downstream consequences of older software architecture and accumulated tech debt — not simply commercial decisions.

And once operational logic becomes deeply embedded into a platform, migration becomes extraordinarily difficult.

Viewed through that lens, this also appears to be an engineering acquisition.

As pressure rises on healthcare SaaS vendors to adapt faster — operationally, architecturally, and increasingly through AI-assisted development and workflow automation — Calmanac's engineering organization and development approach may give Motivity meaningful advantages in:

- enterprise integration,

- operational iteration speed,

- and workflow adaptability.

The Market Is Quietly Rebuilding Around Connected Infrastructure

Multiple parts of the autism technology ecosystem are converging toward similar architectural pressures:

- PM systems moving upstream into intake and CRM,

- clinical systems expanding into operations,

- RCM vendors expanding into workflow orchestration,

- AI vendors requiring broader contextual datasets,

- and providers constructing operational data stores outside their core platforms.

That convergence reflects a growing realization that autism care organizations cannot adapt effectively if operational context remains fragmented across disconnected systems.

This Probably Is Not the Last Major Platform Realignment

I do not think this acquisition will be isolated.

The ABA platform market is still converging toward enterprise reality. Significant investment entered the space under the assumption that platforms would eventually scale upward into the industry's largest providers.

In practice, that has proven far harder than many expected — pushing vendors toward broader operational ownership, deeper interoperability, stronger enterprise infrastructure, and increasingly unified platform strategies.

And this acquisition may ultimately be remembered less as a practice management deal — and more as another signal that the ABA software market is being rebuilt around enterprise operational infrastructure.